Packing your bags and moving to the United States for university is an incredible milestone, throwing you right into some of the most famous academic hubs on the planet. But behind all that excitement, a pretty intense reality check is waiting for you: the endlessly confusing and ridiculously pricey American medical system. If you are preparing to make this massive move, the single biggest question that is probably keeping you up at night is quite simple:

How much does student health insurance cost in the USA? Here at mystudynest, we completely understand that keeping your physical health protected while managing a razor-thin college budget feels like a stressful tightrope walk. This deep-dive breakdown will clear up all the confusion surrounding medical expenses, look closely at your primary options, and give you a straightforward roadmap to lock down the best student health insurance in USA without wiping out your entire savings.

Why is Health Insurance Mandatory for Students in the USA?

The moment your flight lands in America, you will quickly realize that their healthcare setup is a completely different beast compared to what you are used to back home. They don’t have universal healthcare or free public clinics to fall back on if you catch a bug. To be totally honest with you, just dropping by a neighborhood doctor’s clinic for a quick checkup can easily run you anywhere from $150 to $300 out of pocket. And heaven forbid you run into a serious accident that lands you in a hospital bed for a single night—that alone can trigger a massive bill crossing the $10,000 mark before you even realize what is happening.

Because these random medical emergencies can cause total financial ruin for a family, higher education institutions do not mess around. They make carrying an active insurance policy an absolute rule before you are even allowed to step onto a campus property. Outside of university policies, the federal government enforces its own hard laws depending on your documentation. If you are entering on a J-1 exchange visa, the U.S.

Department of State legally requires your insurance to hit highly specific coverage benchmarks. While F-1 visa holders don’t face a rigid national mandate from the government, individual schools handle things via their own internal strict regulations. If you fail to get your international student health insurance sorted out ahead of time, the school will flat-out block you from enrolling in your semester classes.

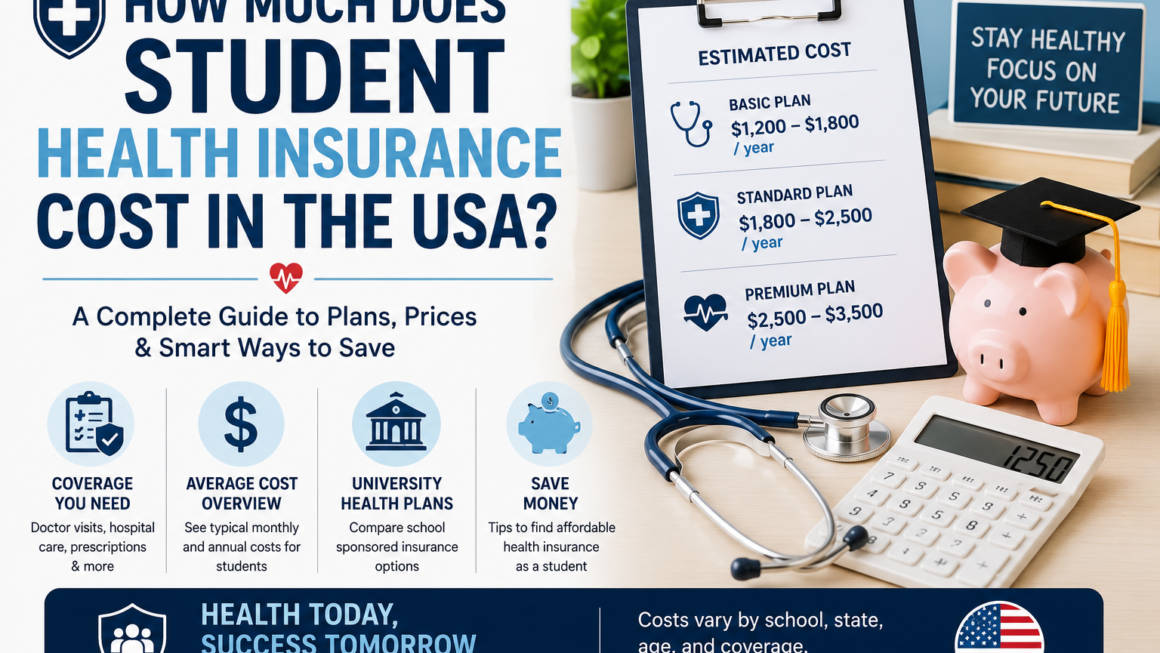

The Average Cost of Student Health Insurance in the USA

So, what is the actual damage going to look like for your bank account? The short answer is that there is no fixed, one-size-fits-all number. Your actual premium will shift up and down based on your school’s exact location, your age, the state’s medical laws, and how much protection you want. Looking at the broader picture, a typical college student can expect to spend somewhere between $1,500 and $6,000 per year to keep themselves covered.

To see exactly where your cash goes, let’s look at the three main routes students take to get insured:

1. University-Sponsored Student Health Insurance Plans (SHIP)

Most colleges will automatically bundle you into their official Student Health Insurance Plan (SHIP) the very second you finish registering for classes. These plans are designed specifically to integrate seamlessly with your campus clinics and local hospital networks.

- Average Cost: Generally lands between $2,000 and $4,500 per academic year.

- The Good Side: Complete peace of mind, fully covers pre-existing or chronic illnesses, and guarantees 100% compliance with your school’s rules.

- The Downside: It usually costs a substantial amount more than searching for a plan on the open market.

2. Private International Student Insurance Plans

If your university leaves the door open for outside choices, you can completely opt out of the school’s default coverage and buy a plan from an independent, specialized provider instead.

- Average Cost: Roughly $500 to $2,500 annually (which breaks down to an easy-to-manage $45 to $200 a month).

- The Good Side: Incredibly light on your wallet, and you can pick different tiers based on your actual budget.

- The Downside: You are completely responsible for navigating the university’s official student health insurance waiver process. If your private policy misses even a tiny detail of what the school requires, they will reject it instantly.

3. ACA Marketplace Plans

For domestic American students—or international scholars who have stayed long enough to qualify as resident aliens for tax purposes—the state or federal Affordable Care Act (ACA) health insurance marketplace becomes an option.

- Average Cost: Highly dependent on your annual part-time earnings, shifting anywhere from $100 to upwards of $500 monthly.

- The Good Side: Low-income students often qualify for heavy government tax credits that slash monthly rates.

- The Downside: The enrollment windows are incredibly narrow, and these policies sometimes do not cover the basic treatments you get at your on-campus student health center.

Key Factors That Determine Your Insurance Premium

When you look closely at how much does student health insurance cost in the USA, you notice that your baseline fee—known as your health insurance premium—is shaped by a handful of core variables:

| The Cost Driver | What’s the Catch? | Direct Impact on Wallet |

| University Location | Medical operations and living costs in hub states like New York, California, or Massachusetts are notably steep. | Expect much higher premiums if your school is in a major coastal city. |

| Age of the Student | Actuaries look at age groups mathematically. The older you are (especially post-26), the higher the statistical risk profile. | Rates scale up steadily as you get older. |

| Deductibles & Copays | Your upfront out-of-pocket setup. Deciding to pay a bit more when visiting a doctor drops your starting cost. | A higher initial deductible always drops your recurring premium. |

| Dependents | Bringing your partner or kids along with you to share your American study journey. | Multiplies the overall cost of the policy exponentially. |

Essential Insurance Terms Every Student Must Know

The American insurance space uses a lot of confusing terminology designed to trip you up. If you don’t grasp these terms early on, you can end up with a massive surprise bill after a routine checkup. Here are the definitions you actually need to remember:

- Premium: This is your basic membership fee. It’s the recurring price you pay every single month or semester to keep your policy active and running.

- Deductible: Think of this as your starting barrier. This is the exact dollar amount you have to pay completely out of pocket for your medical care before the insurance company starts covering a single cent. A $500 deductible means the first $500 of medical work is entirely on you.

- Copay (Copayment): A fixed, flat charge you fork over on the spot every time you use a specific medical service. For instance, you might face a set $25 fee each time you need to pick up regular prescription drugs or see a specialist.

- Coinsurance: Your percentage-based split of a medical bill after you have fully cleared your deductible. If your policy layout is an 80/20 split, your insurance company handles 80% of the cost, and you are billed for the remaining 20%.

- PPO Network: This stands for Preferred Provider Organization. Insurance brands sign specific price deals with local medical professionals and facilities, creating a web of in-network providers. Sticking strictly to these doctors keeps your costs incredibly low compared to going out-of-network.

University Plan (SHIP) vs. Private Insurance: Which is Better?

Weighing the school’s default insurance against an independent third-party plan is easily the biggest choice affecting your personal finances. Let’s break down exactly when each path makes sense.

When to Stick with Your University SHIP

Sticking with your school’s default plan is a no-brainer if your main priority is keeping things simple and hassle-free. These university policies are explicitly built to be ACA-compliant student health insurance.

That means they legally cannot skimp on essential care—they cover mental health counseling, preventative checkups, complex treatments, and long-standing pre-existing conditions without setting any lifetime limits on what they will pay out. An added bonus is that the school drops this charge straight onto your university ledger, meaning you can easily cover it using student loans or financial scholarships.

When to Shop for Private Student Insurance

If your primary goal is finding the absolute most cheap health insurance for international students, independent market providers are your best bet. Companies like ISO, Student Medicover, and Lewerglobal design specific student packages that cost a mere fraction of what universities charge.

However, you have to be incredibly meticulous. You must ensure that the private option perfectly satisfies your school’s health insurance waiver criteria. If the policy lacks even a single minor requirement—like a specific minimum for emergency medical evacuation or a low enough out-of-pocket cap—your university will reject your waiver form, and you’ll be forced to buy their pricey plan anyway.

Hidden Healthcare Costs to Watch Out For

The real cost of staying healthy in America goes way beyond just your premium payments. Countless students get caught off guard by hidden fees because they didn’t dive deep into the fine print of their coverage.

1. Out-of-Network Penalties

If you accidentally visit a clinic, specialist, or urgent care facility that doesn’t have an active contract with your insurer, you might be forced to settle the entire bill alone. Before you ever schedule an appointment, log into your provider’s online dashboard to verify that the doctor is registered as an approved in-network PPO provider.

2. Services Not Covered (Exclusions)

Standard, entry-level student health policies almost never wrap routine dental work or vision checkups into their core plans. If you need standard teeth cleanings, eye exams, new contact lenses, or a fresh pair of glasses, you’ll need to look into buying standalone dental and vision care add-ons.

3. Emergency Room (ER) Fees

Running to a hospital Emergency Room for minor ailments like a bad cold, a mild sprain, or a random skin rash is a massive financial mistake. ER visits often carry an automatic baseline copay ranging between $200 and $500. Unless you are dealing with a true, life-or-death situation, popping into a nearby urgent care clinic or your campus wellness center will save you a massive amount of cash.

Step-by-Step Guide: How to Apply for a Health Insurance Waiver

If you have run the numbers and decided that buying a private plan is the absolute best way to protect your budget, here is the exact step-by-step process to opt out of your school’s default plan:

- Pull up the Requirements Checklist: Go to your university’s student health portal and print out the exact list of conditions an outside plan must meet.

- Shop and Compare Carefully: Look through reputable private insurance sites and pick a plan that explicitly guarantees it aligns with your specific university’s waiver rules.

- Buy the Plan Early: Finalize and buy the private policy before your school semester officially kicks off so you have your digital insurance cards and policy text ready to go.

- Submit Your Waiver Form: Head back into your school’s student dashboard, open up the health waiver portal, type in your new policy details, and upload your proof of coverage.

- Keep tabs on your Student Bill: Once you get the official approval email, look closely at your university tuition invoice to make sure the massive university insurance charge has been completely wiped off your balance.

Summary: Top Tips for Saving Money on Student Healthcare

- Make Your Campus Clinic the First Stop: Most schools run their own on-campus clinics that offer free or incredibly low-cost routine checkups, mental health support, and vaccinations, regardless of your insurance provider.

- Always Stay In-Network: Take a minute to check your insurer’s app before a medical visit to confirm that the clinic, doctor, and pharmacy are fully in-network.

- Look Into State-Level Subsidies: If you are a domestic student working a part-time job or a graduate teaching assistant with a stipend, you might qualify for state Medicaid or regional marketplace discounts.

- Avoid Buying Based Solely on Price: A dirt-cheap policy usually means sky-high deductibles or zero protection for major health crises. A plan that leaves you exposed in a real crisis is a complete waste of money.

Locking down the right health policy is just as crucial as selecting the right classes for your major. By taking a little time to weigh your school’s SHIP against certified private options, you can insulate both your physical health and your hard-earned finances—leaving you free to focus entirely on crushing your academic goals in the USA.